Draft European Sustainability Reporting Standards

By Julia Staunig, Senior Managing Director, Teneo & Ramona Visenescu, Consultant, Teneo

On 29 April, the European Financial Reporting Advisory Group (EFRAG), the advisory body in charge of developing the EU’s sustainability reporting standards, published the first set of draft European Sustainability Reporting Standards (ESRS) for consultation. The draft gives a first glimpse of what companies might have to report on according to the Corporate Sustainability Reporting Directive, i.e. the updated EU rules for which companies need to report non-financial information and in which form.

Importantly, the standards are based on the principle of double materiality. This means that companies will need to disclose information on how ESG risks impact their business and their externalities, i.e. how their activities impact the environment and stakeholders. With that, the EU goes further than other frameworks, including the International Sustainability Standards Board (ISSB), which bases its work on the perspective of financial materiality only.

Summary of the Draft ESRS

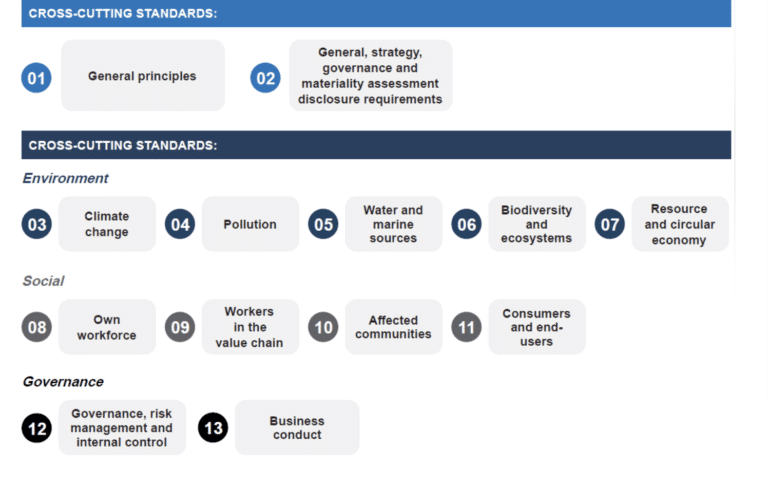

The Draft ESRS are divided into 13 chapters, each covering a different aspect of sustainability:

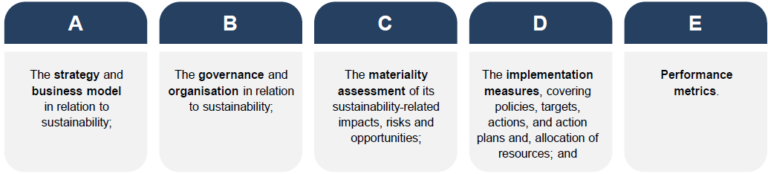

The provisions are sector agnostic, i.e. they set disclosure requirements relating to sustainability impacts, risks and opportunities that are deemed material for all companies, regardless of the sectors in which they operate. Companies are required to disclose information related to the following areas:

The provisions are sector agnostic, i.e. they set disclosure requirements relating to sustainability impacts, risks and opportunities that are deemed material for all companies, regardless of the sectors in which they operate. Companies are required to disclose information related to the following areas:

Draft European Sustainability Reporting Standards

The first three reporting areas are covered by the cross-cutting standards since they are relevant for all sustainability-related topics.

The last two reporting areas are covered by the topical standards. The topical standards are the ones related to specific ESG elements. These provisions set disclosure requirements related to:

- Environment, such as disclosures on climate change adaptation and mitigation, targets for resource use and circular economy, and measurable targets for pollution;

- Social, such as disclosures on the process for engaging with own workers, training and skills development indicators, value chain workers, and policies related to affected communities and;

- Governance, such as disclosures on business conduct culture, prevention and detection of corruption and bribery, and risk management processes.

Some of the targets and performance measurement metrics in the provisions, especially the ones related to climate, correspond to other, internationally established standards, such as the ones prepared by the Task Force on Climate-Related Financial Disclosures (TCFD) and ISSB.

Governance Process for Drafting the ESRS?

As noted above, EFRAG is an advisory body set up to guide European corporate reporting rules. Initially created for the purposes of facilitating the process of endorsing financial reporting standards for EU use, EFRAG’s remit has now been extended to cover the creation of non-financial reporting standards on the basis of relevant international frameworks. Formally, EFRAG’s drafts need to be adopted by the European Commission as so-called “delegated acts”. There is also an element of political oversight in this process, with the European Parliament and Council (i.e. EU Member States) having the right to veto the Commission’s implementing acts.

Next Steps

EFRAG’s public consultation runs until 8 August 2022, and the stakeholders’ feedback will inform the standards that EFRAG will suggest to the European Commission in November 2022. The European Commission will then have to endorse the standards by the end of 2022.

In addition to the drafts described above, EFRAG will prepare sector-specific standards, which will include provisions that are material for companies in specific sectors. These provisions are to be adopted by the Commission at a later stage.